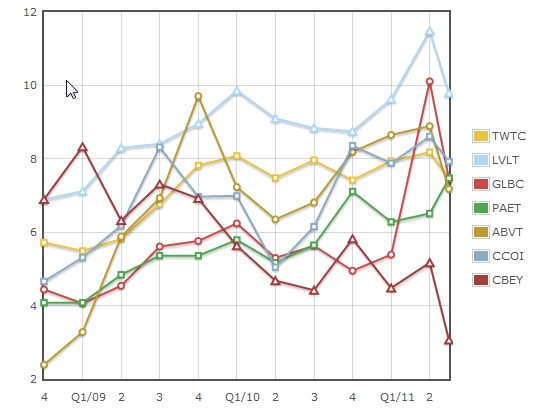

The third quarter has not been a fun one for investors in US competitive network operators, despite the fact that operationally the sector continues to do just fine. Below I’ve cribbed a static relative valuation plot of EV/EBITDA(ttm) from my Competitive Telecom Trends pages, the final datapoint of which reflects current stock prices as we approach the end of the third quarter:

You can find the interactive version here. The recent downtrend is obvious, especially when one realizes that the only valuation to rise since June 30 is PAETEC, whose number benefits both from the August purchase by Windstream and the fact that its trailing twelve months of EBITDA doesn’t yet reflect their run rate due to their own M&A activity.

Level 3’s valuation has given back all the anticipated Global Crossing synergies, but is now the only one still above 8 on this chart. Any premium AboveNet was getting from those M&A rumors over the summer is more than gone, while Cogent and tw telecom have lost less ground. CBeyond hasn’t had a valuation this low since I’ve been collecting data.

The overall uptrend in market opinion of fiber assets that we have seen in the past two years isn’t in danger quite yet, but it seems clear that the honeymoon is over for now. That also helps explain the lack of fiber-related M&A over the summer despite the fact that we know there was a lot of it in play. The prices being asked swiftly became too high, and since the sellers were mostly opportunistic to begin with the opportunity just vanished.

Yet growth trends continue to be better than the overall market, and EBITDA margins are still trending upward for those with the most fiber in their diet at least. If indeed we are on the cusp of another rough economic stretch, the industry as a whole appears to be well positioned for it.

If you haven't already, please take our Reader Survey! Just 3 questions to help us better understand who is reading Telecom Ramblings so we can serve you better!

Categories: CLEC · Financials · Metro fiber

Rob, This remains a great chart and tool! It’s interesting that the (3)/Global Crossing post merger synergistic ebitda develops into a ratio of 7.1-7.2 once plotted for.

Oh yes, one add on to my ratio comment would be “according to today’s market prices” from both securities which had occurred from an out in left field bullish analyst turn bearish on the macro scene over at DAD.

These combined two quotes represents a .69 P/S based upon the most conservative revenues of both companies being melded together.

You pay a dirt cheap price for such dreary consensus.