One of the first questions that springs up in looking at this deal is whether Level 3 really ought to be taking on another integration after the well known troubles they went through in 2007-2008. Actually, there are a number of reasons why this one should be much easier:

- Cleaner asset fit – Much of Level 3’s troubles the last time around came from two sources: the mismatch in the customer bases with Broadwing, and a plethora of differently run but physically intertwined metro assets. Global Crossing’s local assets in South America and the UK outside of London will need little integration, as they are independently run and have no geographical corollary at Level 3. The US and continental European assets are mostly longhaul, which is less messy and more familiar. The multinational corporate business of Global Crossing can also be swallowed mostly whole. And the US backbone of Global Crossing lies on the original Qwest build just as Genuity’s once did – they are quite familiar with it.

- Equipment compatibility – Global Crossing’s backbone of today has a pile of Infinera gear in it, as does Level 3. That contrasts with Broadwing’s former Corvis gear, for example, which was an entirely different beast. Of course, Level 3 has been said to be transitioning from Infinera gear to Huawei, but nevertheless most of the existing gear is probably quite compatible.

- Fewer skeletons in the closet – While you won’t hear it from them (keep it simple), Level 3’s previous speed bumps were more than simply integration issues. A whole barnyard of other chickens came home to roost when things went south, which is part of why it took so long to work through. While that process was not any fun, the demons of the past have been largely exorcised.

- Global Crossing has some integration expertise too – While Level 3 will have to prove its skill at integration again, Global Crossing has a rather good track record in this regard. They integrated both FiberNet in the UK and Impsat in South America without a hitch, and thus far things seem to have gone well with Genesis Networks.

That’s not to say such an integration will be a piece of cake, these are two multi-billion dollar companies with more than five thousand employees each spread around the world. Anytime you take on a task that large, there are plenty of risks. But on some levels, really is more straightforward this time.

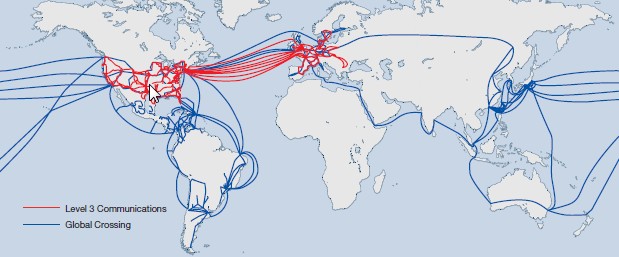

Here’s the map from today’s presentation of the combined assets:

If you haven't already, please take our Reader Survey! Just 3 questions to help us better understand who is reading Telecom Ramblings so we can serve you better!

Categories: Internet Backbones · Mergers and Acquisitions

I see a lot of GC’s guys departing

such amount of sinergies will came from GC guys

Yes that is how it will be, besides GLBC staff has more ‘expertise’ in the layoff process than LVLT

The thing I don’t understand is how Level 3 is allowed to take on additional debt? I fully understand that Patel is great at savvy dealmaking, but at some time isn’t Level 3 going to have to pay the piper? Am I missing something Rob?

It’s not about how much raw debt, but rather how much debt can a company’s operations support. After synergies, this deal actually makes LVLT’s debt smaller relative to what the combined operations can support.

As for paying the piper, they do that every time a bond comes due or gets refinanced. The key is finding another piper willing to lend more, and thus far Sunit has been a master at it. As long as they don’t screw up the integration here though, a debt/ebitda ratio will mean the piper won’t be so agitated any longer and it will only get easier.

DEBTORS JAIL, i think this is a great point. the combined company will have a mountain of debt. Rob, read your Hyman Minsky. This is a classic Minsky moment caused by the Fed’s QE1 & QE2.

Patel has demonstrated that he is an incredibly capable CFO, but even the best juggler eventually drops a ball, especially when more and more are added to the act.

eventually interest rates go up. I suggest you look at the term structure of the combined company’s debt before you quote a simple ratio cited in the powerpoint slides they created for this transaction.

I offer a very rudimentary example. A Debt to EBITDA ratio does not account for higher interest rates. 10b in debt and 1.1b in EBITDA might mean you can service your debt at 10% interest. but what happens when that 10b is financed at 12% or 14% or 15%? Your all-important debt to ebitda ratio remains the same (remember the I in EBITDA means before interest expense) but you can no longer service that 10b of debt.

You have no clue what you are talking about. Your rudimentary example makes no sense. When your ratio of debt to EBITDA drops (either because your debt is lower or your EBITDA is higher) your debt premium drops (i.e. the interest rate premium you have to pay over treasuries). That means your cost of capital drops.

In other words, people with little debt relative to their income pay much lower interest rates than people with high ratios of debt/income.

Referencing Hyman or Misky in here is like using a calculus textbook to figure out your taxes… completely irrelevant… and comical.

ok, so why do interest rates on treasuries go up? We have a printing press in this country so we can always pay our debt. i’m pretty sure the interest rate on 10 year treasuries has not been constant over our history. (If you think it has you can stop here.)

I am pretty sure inflation expectations play a small little role in the level of interest rates. When treasuries go up so do interest rates on all other debt. A small improvement in EBITDA will not lower your interest rate enough to offset a large change in treasury interest rates due to a change in inflation expectations.

My point is quite simple: DEBT to EBITDA alone is not sufficient to gauge a company’s ability to service it’s debt. If you think it is, I believe level 3 has some debt to sell you.

In corporate finance you really only look at your credit spread… not at the base rate (i.e. treasuries). Treasuries rates are externalities, you have no control over those. As a CFO, your job is to lower your costs of capital over the variables you can control. And your most basic variable in determining your spread is Debt/EBITDA.

If you are fearful about base rates, you can always hedge those. No big deal. Refusing to borrow just because “borrowing is a bad thing” will likely keep you from funding growth for your company and your firm will end up with an awfully inefficient and expensive capital structure (the intrinsic cost of capital on your equity is also dependent on your treasury rates and much, much higher than that of your borrowings). In which case your CEO/board might as well fire you for ignorant and incompetent.

I will not get in a discussion over future treasury rates in here. I have no crystal ball over what those are going to do in the future… if you believe so strongly the US is just about to go down the tubes and interest rates will go through the roof I suggest you open a futures account and place an incredibly levered bet on interest rates. You should also short the dollar… and probably the rest of US markets. If you are right you will become incredibly wealthy. Really. At this point the markets overwhelmingly agree rates are going to stay low for a very long time. But you might be smarter than everyone else.. and beat the capital markets at their own game.

great reply. as i read the debt comments that you were responding to, my jaw dropped at the lack of understanding.

Wrong again, Rob! GC has not integrated the Impsat network at all. They run completely different systems, and actually, truth be told, have a terrible track record at working with the ROW. But if you were the insider you claim to be, you would already know this.

One thing is for sure, Legere will make millions, yet the employees will be the losers.

Do your homework, Rob!

he did his homework. he asked the executives and they told him they are integration experts. Good enough for me.

If he asked executives at GC, then they lied, which will present more issues than outlined.

What executives made such a statement, because I know the facts and IMPSAT is a separate network STILL, 3 years after the fact.

Impsat

Sat stands for satelitte,25%/ 30% of their revenues came from satellite , they have lost a big chunk of the Brazilian satellite market to Hughes service , that took the opportunity to provide services when GC decide not to invest any more in new satellite equipment, what they lost

U$S 50 mill only in Brazilian market and eventually they los another 20 mill in Latam, remembering that Impsat was the Leader and “the only one” on that market.

Impsat own and operates 16 DC which generates aprox u$s 150 millions annual revenues

Integrated or not is a complete different business that has generated, the largest GC’s “growth” engine

The largest EBITDA contributor , the only business unit with positive eps contribution

A business Model that the top GC’s guy never looked after , their incentives were designed to sell de company not to manage the company , of course they did what they were incentivized 80 mill for 5 guys is not bad and 40 mill for JJL is enough clear were they put their focus.

Good Job(for the board!!!)

Bad for shareholders in 2007when they bought impsat GC was 23/24 u$s per share.

Result is more than obvious at least for me, even I don’t Like “the marathon runner” was Board decision not his.

Windstream wants to be a national player vs. a ‘multi-regional’ player which they are today. Nuvox billing platform should help out as foundation to build on. Buying Nuvox fills in the southeast, Telepacific would be a great fit for them in the west.

I think you also have to consider the executives in charge of each company. I can’t imagine the crew at the top of GC going quietly.

The cultures of the two companies are completely different, too. And will Level3 be able to overcome its wholesale inertia to embrace global enterprise services? Seeing how hard it was and how long it took for GC, I’m cynical.

Rob, have you put a pencil to how many of the > 10K names will be seeking gainful employment after this deal is done?

My back of the envelope number is 2300 based upon the average revenue per ee at 65K, and extrapolating 1/2 of the opex synergies discussed.

In order to be less painful, higher income related employees will have to go.

By the way, with rare exception those who attempted to discuss the DEBT/EBITDA ratio concept along with how corporate interest rates are developed not to exclude a significantly better “credit profile” tied “rating agency” upgrades, must study harder.

The first question they might ask themselves to counter their brain spasm, is how and why would LVLT have what on some “tranches” amounts to “usury,” i.e., fifteen percent, during what continues to be the lowest interest rate period in the HISTORY of MODERN FINANCE!

Check that for one second, Rob. Yesterday, I did the number in my head while 1/2 napping understanding that RIF was going to be 70 percent worth of 1/2 the opex synergies according to Sunit and using 100K average ee salaries which led me to about 1,500 pink slips. Sorry, unless it’s going to be Anonymous who gets the axe for filling your board with brain farts on “the price” of corporate “funds” in front of this deal.