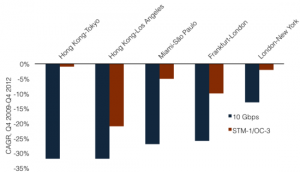

According to the telecom research firm Telegeography, 10G waves on major international routes saw substantial price cutting last year. Between Q4/2011 and Q4/2012, their data say that median monthly prices for 10G waves between major global markets fell some 37%, while pricing for smaller pipes was somewhat more stable.

While carriers are all looking ahead to 100G deployments, 10G waves will continue to be the industry workhorse for some time to come. With pricing still falling so easily, one wonders just how long it will really take before 100G’s economics really justify the upgrade for most of the industry.

While carriers are all looking ahead to 100G deployments, 10G waves will continue to be the industry workhorse for some time to come. With pricing still falling so easily, one wonders just how long it will really take before 100G’s economics really justify the upgrade for most of the industry.

The greatest pricing pressure came to and within the APAC region of course, as the capacity from all the new cables continues to drive overall pricing closer to that in the western hemisphere. But it’s interesting that Telegeography also saw Miami-Sao Paolo prices drop by some 27% and Frankfurt-London by nearly as much, while the transatlantic route (London-NYC) was rather more stable.

Of course these are some of the internet’s most competitive links, I wonder what pricing has looked like on the somewhat less traveled routes.

If you haven't already, please take our Reader Survey! Just 3 questions to help us better understand who is reading Telecom Ramblings so we can serve you better!

Categories: Internet Backbones · Internet Traffic

or what impact the new Hibernia, Emerald, etc. cables will have when (if) completed. All of that stuff in the south Atlantic will surely have an impact on the north Atlantic routes as providers shift to more optimal routes.

Hibernia isn’t happening

Can I just say what a relief to find someone who actually knows what they are talking about. You definitely know how to bring an issue to light and make it important. I cant believe you are not more popular because you definitely have the gift. Everything about Hostwinds – http://hostwindsreview.tumblr.com/